Faith Nyasuguta

For nearly half a century, the sovereignty of the European wallet was an illusion. From the bustling kiosks of Paris to the high-end boutiques of Milan’s Via Montenapoleone, the act of “paying” was effectively an American export. Every time a European consumer tapped a piece of plastic or scanned a digital wallet, a silent, invisible signal traveled across the Atlantic to servers in Missouri or Virginia. There, two titan corporations -Visa and Mastercard – acted as the high priests of the transaction, validating the exchange, harvesting the data, and clipping a microscopic but multibillion-dollar coupon from the continent’s GDP.

This was the “Great Convenience,” a system so efficient and so deeply embedded that it felt like a natural law. But in the corridors of Brussels and the boardrooms of Frankfurt, the realization has finally set in: a continent that does not own its own payment rails is a continent that does not truly own its own economy. Today, in early 2026, the breakup is no longer a theory. It is a cold, calculated “uncoupling” – a systematic effort by the European Union to build its own financial plumbing and finally move the American giants out of the center of its domestic life.

The Hidden Cost of Dependency

To understand why Europe is leaving, one must look at the sheer scale of the rent it has been paying. For decades, the European banking sector operated in a state of comfortable subservience. While local banks issued the cards, they were almost entirely reliant on the “rails” provided by Visa and Mastercard. These two companies did more than just move money; they set the rules. They determined the interchange fees that squeezed small merchants and controlled the behavioral data of millions.

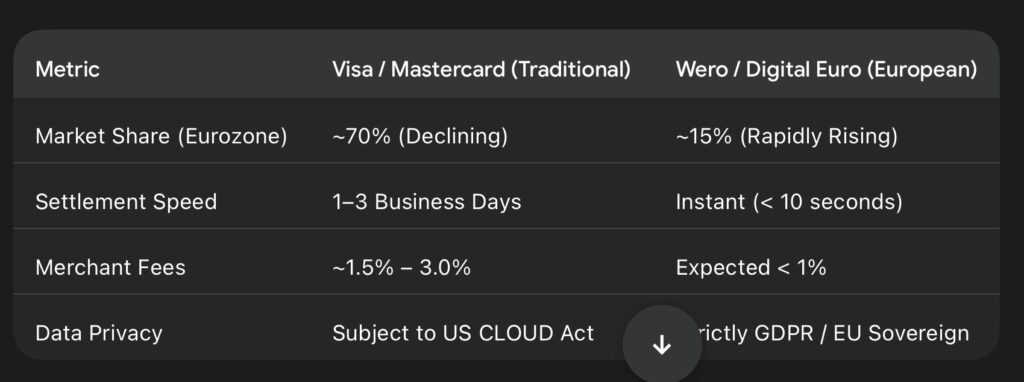

The data reveals a staggering imbalance. As of 2025, Visa and Mastercard still controlled approximately 70% of all card transactions across the Eurozone. In the second half of 2024 alone, card payments in the Euro area reached a massive 1.7 trillion Euros. Because these networks are headquartered in the U.S, a significant portion of the fees and all the metadata associated with these trillions of euros sits outside European legal jurisdiction. For a bloc that prides itself on “Strategic Autonomy,” this was a structural trap.

The Geopolitical Wake-Up Call

While the desire for independence was brewing for years, the geopolitical earthquake of 2022 turned a policy goal into an existential necessity. When Russia invaded Ukraine, the world witnessed the terrifying efficiency of financial warfare. Within days, Visa and Mastercard suspended operations in Russia. Almost overnight, cards became dead plastic.

For European leaders, this was a mirror. They realized that if a diplomatic rift ever opened with Washington -over climate, tax, or trade -the U.S. possessed the “kill switch” for the European economy. Martina Weimert, the CEO of the European Payments Initiative (EPI), put it bluntly: “Europe urgently needs to reduce its reliance on non-EU payment rails.” The lesson was clear: you cannot be a global power if your citizens cannot buy bread without the permission of a foreign company.

Wero: The Homegrown Challenger

The spearhead of the counter-offensive is Wero. Launched by a coalition of 16 major European banks, Wero is the EU’s attempt to build a “Sovereign Rail.” Unlike Visa and Mastercard, which use card numbers and complex middle-layers, Wero is built on SEPA Instant Credit Transfers. It moves money directly from one bank account to another in less than ten seconds.

The growth of Wero has been explosive. By February 2026, the platform reached 43.5 million registered users in its first year across Germany, France, and Belgium. It has already processed over 100 million transactions, totaling more than 7.5 billion Euros.

The strategy is simple: start with “lunch money” (peer-to-peer transfers) and move to the “big money” (online shopping and in-store payments). In 2026, Wero is rolling out its e-commerce functionality, allowing consumers to pay major retailers like Air France and Orange without ever touching a U.S. card network. For merchants, the math is irresistible: while credit card fees can range from 1.5% to 3%, Wero aims to offer a significantly cheaper, instant alternative.

The Trillion-Dollar Threat

The financial implications for the American incumbents are severe. Analysts are now predicting that a successful shift to Wero and other local systems could lead to trillions of dollars in lost transaction volume for Visa and Mastercard over the next decade. As the Netherlands migrates its dominant iDEAL system over to the Wero platform in 2026, an entire national payments market is effectively being delivered to the European system.

To reinforce this, the European Central Bank (ECB) is advancing the Digital Euro. On February 10, 2026, the European Parliament voted to back the digital currency for a 2029 launch. The ECB’s goal is to ensure that “Europe controls its financial destiny” by providing a public, state-backed alternative to private U.S. networks.

The Shift in Power (2026 Forecasts)

A Future of Optionality

The “Quiet Breakup” is not about a sudden ban on American cards; it is about ending a monopoly. For the foreseeable future, Visa and Mastercard will remain essential for global travel and high-end credit. However, for the daily life of a European – buying groceries, paying rent, or shopping online – the “Priceless” era of American dominance is being cashed out.

As Piero Cipollone of the ECB Executive Board noted, a digital, sovereign solution will “enhance the resilience of Europe’s payment landscape and lower costs for merchants.” Europe isn’t just changing its apps; it is changing the very rails that its society runs on. The locks have been changed, and the quiet eviction is well underway.

RELATED: